Imagine having insider access to groundbreaking scientific research, defense contracts, or upcoming economic policies before anyone else in the market. Now, imagine being able to trade stocks based on that privileged information, potentially making millions. This isn’t a fantasy for some; it’s a very real concern fueling a fiery national debate about ethics and transparency within the halls of Congress.

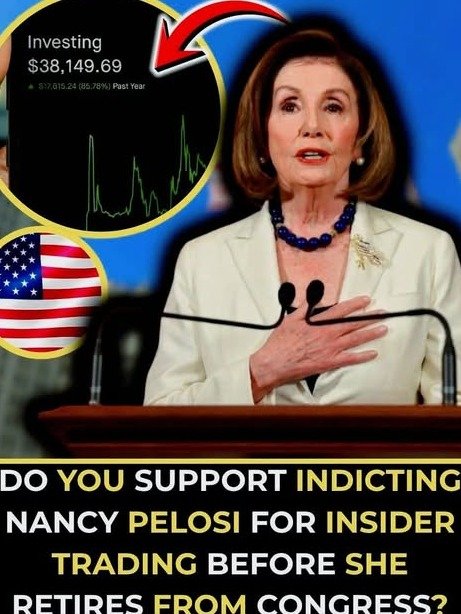

For years, a simmering tension has existed between the public’s expectation of integrity and the financial activities of its elected officials. High-profile figures, including former House Speaker Nancy Pelosi, have found their stock trades—or those of their spouses—under intense scrutiny. These transactions often raise questions about whether lawmakers are leveraging their unique positions for personal financial gain.

The Blurring Lines of Power and Profit

At the heart of this controversy lies a fundamental conflict of interest. Members of Congress are privy to a vast array of sensitive information that can directly impact market trends and corporate valuations. They vote on legislation, oversee regulatory bodies, and receive briefings on everything from international relations to emerging technologies.

This privileged access creates an inherent advantage, allowing them to potentially make highly informed, and often incredibly lucrative, investment decisions. The concern isn’t just about outright illegal insider trading, but the mere appearance of impropriety that erodes public trust in democratic institutions.

When lawmakers trade stocks, particularly in sectors directly affected by their legislative work, it creates a perception that the system is rigged. Citizens often wonder if policy decisions are being made in the best interest of the nation, or to line the pockets of those in power.

High-Profile Scrutiny: The Pelosi Effect and Beyond

Few figures have drawn as much attention to this issue as former House Speaker Nancy Pelosi. While she herself does not directly trade stocks, her husband, Paul Pelosi, has made numerous high-value trades that have sparked widespread public debate. These transactions have often coincided with legislative developments or significant economic news, leading many to question the timing and potential informational advantage.

For example, trades involving tech giants or semiconductor companies, made shortly before crucial votes or announcements affecting those industries, have fueled public suspicion. While no direct evidence of illegal activity has been proven, the optics alone have been enough to ignite a firestorm of criticism and calls for stricter regulations.

However, the issue extends far beyond one individual. Numerous other members of Congress from both sides of the aisle have faced similar accusations regarding their own or their family’s stock trading activities. These instances collectively paint a picture of a system that, at best, lacks sufficient safeguards, and at worst, permits a subtle form of legal corruption.

Understanding the Current Rules: The STOCK Act

In response to growing public outcry and a series of investigative reports, Congress passed the Stop Trading on Congressional Knowledge (STOCK) Act in 2012. This bipartisan legislation aimed to increase transparency and prevent insider trading by members of Congress and their staff. It explicitly affirmed that existing insider trading laws apply to federal lawmakers and employees.

The STOCK Act’s key provision requires members of Congress to publicly disclose any stock trades made by themselves, their spouses, or dependent children within 45 days of the transaction. This disclosure is meant to provide transparency, allowing the public and watchdog groups to monitor their financial activities.

Furthermore, the Act mandated that Congress establish clear ethics guidelines and strengthened enforcement mechanisms. It was heralded at the time as a significant step towards restoring public confidence and ensuring that lawmakers were held to the same standards as ordinary citizens when it came to financial markets.

Why the STOCK Act Isn’t Enough

Despite its intentions, the STOCK Act has proven to be largely insufficient in addressing the core concerns. Critics argue that its primary focus on *disclosure* rather than *prevention* leaves a gaping loophole. Simply knowing that a lawmaker made a timely, profitable trade after the fact doesn’t prevent the perceived conflict of interest or potential abuse of information.

Enforcement has also been a persistent problem. Fines for late disclosures are often negligible, serving as little deterrent for those making substantial profits. Moreover, the 45-day reporting window, while an improvement, still allows for a significant delay, making real-time scrutiny and accountability challenging.

Many argue that the Act fails to address the fundamental issue: the ability of lawmakers to actively trade individual stocks while simultaneously legislating on matters that affect those very companies. The concept of a